Economic growth, marketing investment, own-brand products: 5 interesting stats to start your week

We arm you with all the numbers you need to tackle the week ahead.

UK shoppers shift spend to own-brand products

With the cost of living and inflation rising, UK shoppers are shifting spend towards supermarket own-label products, with sales of branded FMCG products declining by 5.1% in March.

The share of sales from FMCG private label products has risen from 52.4% last year to 53.2% today. Meanwhile, sales of ambient own-labels products increased by 3.3% in the past four weeks, which Nielsen describes as a “significant change” in a category where brands dominate with 61% of total sales.

Total till sales at UK supermarkets fell by 4.1% in the four weeks ending 26 March, the slowest sales growth recorded in 2022 so far.

Online sales dropped by 19% compared to the same period last year, but the UK was in various stages of lockdown at this point in 2021 and online sales had surged by 92%. In-store sales fell by 0.6% last month, according to the data from NielsenIQ. Store visits rose 5% over the last four weeks, and the overall online share of sales has stabilised at 12.4% versus 14.8% this time last year.

At £18.52, spend per visit across all channels is practically the same as in February when the figure was £18.50.

Source: NielsenIQ

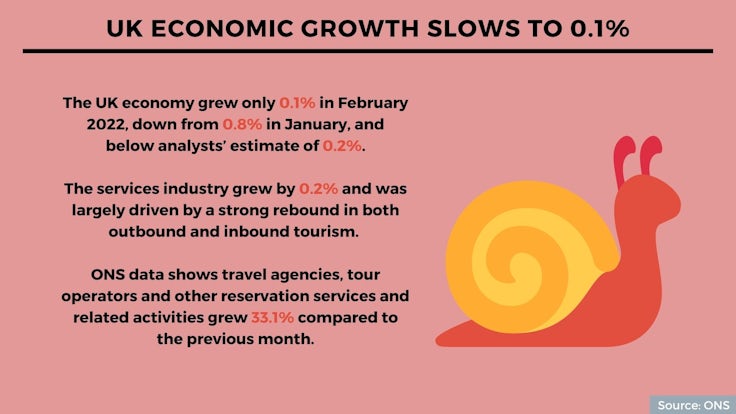

UK economic growth slows to 0.1%

The UK economy grew only 0.1% in February 2022, down from 0.8% in January, and below analysts’ estimate of 0.2%. But GDP is now 1.5% above its pre-coronavirus pandemic level from February 2020.

The services sector was the largest contributor to February’s growth, says the Official for National Statistics (ONS). The services industry grew by 0.2% and was largely driven by a strong rebound in both outbound and inbound tourism. ONS data found that travel agencies, tour operators and other reservation services and related activities grew 33.1% compared to the previous month.

Manufacturing and construction were some of the sectors that contributed to the lower-than-expected growth in February 2022. Production output fell by 0.6% in February 2022. Manufacturing was the main driver of negative growth, falling by 0.4%.

Meanwhile, construction output decreased by 0.1% in February 2022 following growth of 1.6% in January 2022. However, this output remains 1.1% above its pre-coronavirus pandemic level in February 2022.

The ONS says that factors like the impact of storms Dudley, Eunice and Franklin, which all hit the UK between 16 and 21 February, may have also weighed on economic growth that month.

Source: ONS

Global marketing investment to grow 30% by 2025

Global marketing investment is expected to grow 30% by 2025, an increase of $4.7trn (£3.5trn).

Despite the impact of the pandemic, an estimated $3.6trn (£2.6trn) was spent by public companies on marketing in 2021. Spend was therefore up 13% on 2020 and 2% on 2019, indicating a rebound in marketing investment as pandemic restrictions have lifted.

According to the forecast by Forrester, the ability to measure the return on investment (ROI) of digital marketing will be helping to justify this greater spend to chief financial officers. Performance marketing saw the most growth in 2021.

Meanwhile, changes to consumer behaviour post-pandemic will boost marketing’s importance moving forward, whether that be in retaining customers, recapturing old customers, or enticing new ones.

However, the UK is expected to see the second slowest growth rate in marketing spend between 2021 and 2025, at 2.7%. The UK spent an estimated $158bn (£120bn) on marketing in 2021, the seventh highest nation behind Japan ($214bn/£163bn), France ($195bn/£149bn) and Germany ($193bn/£147bn).

Only Russia lags behind the UK at a predicted growth rate of 1.4%. The global average is 7%, while China’s and India’s marketing spend will grow the most, at 13.4% and 12.7%, respectively.

Source: Forrester

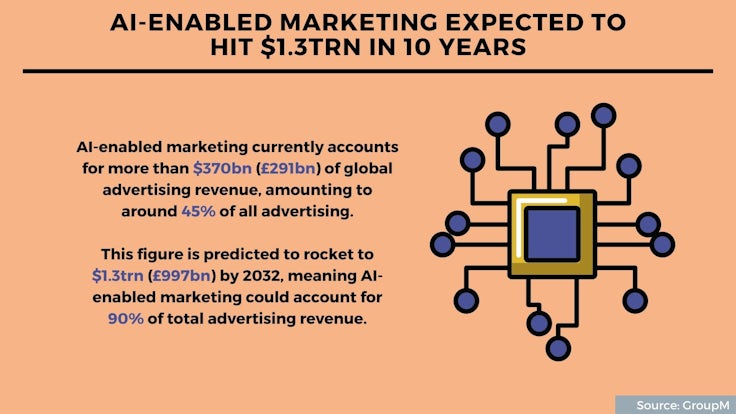

AI-enabled marketing expected to hit $1.3trn in 10 years

AI is expected to be involved in “nearly all internet advertising” in a decade’s time. AI-enabled marketing currently accounts for more than $370bn (£291bn) of global advertising revenue, amounting to around 45% of all advertising, according to GroupM.

This figure is predicted to rocket to $1.3trn (£997bn) by 2032, meaning AI-enabled marketing could account for 90% of total advertising revenue.

Given the rise of AI and widespread adoption of technology and wireless connectivity, GroupM suggests the media landscape will look “considerably different” in 10 years’ time.

Audio, such as smart-home speakers and car audio systems, will see continue to grow in prominence. Voice searches will likely overtake text searches by 2032, where current estimates suggest 10% to 15% of searches are voice-activated. GroupM suggests this will allow for greater personalisation of advertising in shopping results and music.

Meanwhile, TV’s need for a linear reach will no longer be “sufficient to meet most marketer goals”. With the rise of streaming services such as Netflix and Disney+ there will be a global increase in ad-free television.

As ad-free platforms will dominate, GroupM suggests advertisers will need to be more creative to reach consumers. Marketers may instead turn to other video environments, such as YouTube and TikTok, where “consented information” on viewers allows for targeted messages.

Source: GroupM

UK footfall improves further as restrictions are lifted

Footfall is improving gradually as all restrictions in the UK have now been lifted. Total footfall improved by 1.2 percentage points in March compared to the previous month, this is 15.4% down on 2019 pre-pandemic levels but significantly higher (179.6%) than last year.

The BRC-Sensormatic IQ Footfall Monitor data compares all figures to three years ago to provide meaningful comparisons.

While footfall in the UK is still 15.4% lower than in March 2019, it is ahead of other European countries in its recovery, with France (down 25.5%), Germany (37.5%) and Italy (38.6%) all taking longer to return to pre-pandemic levels.

In the UK, shopping centres are still taking the longest time to recover, with footfall down 35.8% compared to March 2019, but this is 4.3 percentage points higher than last month.

High street footfall is up 3.1 percentage points versus February, a decline of 17.8% compared to 2019. While retail park footfall is down 7.3% compared to pre-Covid levels, but up 3.1 percentage points versus last month.

Source: BRC-Sensormatic IQ

Print the article

Print the article